Critical illness insurance is an agreement with a life insurance company where they pay you a tax-free lump sum in the event they contract a life-threatening condition or illness. Unlike term life insurance, critical illness insurance is not meant to provide long-term financial support to your family after you pass away but rather grants financial support while you are recovering from a critical illness.

By Carly Griffin Senior Insurance Advisor, LLQP 27 min read September 14th, 2023 IN THIS ARTICLEGetting critical illness insurance can bring you great peace of mind. Knowing you’ll have a financial safety net should you fall seriously ill can allow for economic flexibility in your future plans and safeguard you and your family against the unexpected.

Maybe your broker told you just the basics about critical illness insurance—”If you get really sick, the insurance company will pay you a tax-free lump sum if you develop a life-threatening illness, health event, or undergo treatment while under their coverage!”

Sounds like a great deal! Sounds like you’ll be taken care of no matter what! Right?

But, what if you were to get sick and then discover that your condition wasn’t covered by your policy? Not only would you be emotionally devastated, but you’d be forced to up-end your finances during one of the most dire times in your life.

That’s why it’s incredibly important to fully understand what conditions are covered by your critical illness insurance policy before purchasing. Not only should you know what’s covered, but you should familiarize yourself with the definitions of each ailment as stated by your insurer. By making sure that you’re covered for all the illnesses you’re most concerned about, and doing your homework on what constitutes a valid claim, you’ll avoid any shock or disappointment should tragedy strike.

But before we dive into the most commonly covered critical illnesses, if you’re not completely sure what critical illness insurance even is, we suggest reading our honest guide to critical illness insurance first.

Call 1-888-601-9980 to speak to our licensed advisors right away, or book some time with them below.

In 2018, the Canadian Life and Health Insurance Association (CLHIA) updated its Critical Illness Benchmark Definitions in order to help standardize the language around common conditions and afflictions across the industry.

CLHIA listed and defined 26 common illnesses, conditions or health events in their publication, but that is not the maximum number of conditions that can or will be covered by an insurance provider. Some insurers may offer coverage for illnesses not defined by the CLHIA and some may even use their own qualifying language.

However, these definitions are commonly used and adhered to by many insurers, so you should familiarize yourself with them before choosing a provider. This is true whether you have a critical illness insurance policy or riders. There are some important distinctions in their descriptions. Whether it’s as broad as specifying coverage is only for bacterial meningitis and not viral, or as specific as the hourly length of time of a coma and its grade on the Glasgow coma scale, this language is ultimately used to determine the validity of your claim and therefore vital to understand.

The 26 conditions that most common carriers cover are:

Please note that not all of these are included in every insurance policy, unless explicitly stated. If you have an existing policy or intend to buy one, please refer to the policy documents for full terms, conditions, and definitions.

Critical illness insurance in its current form was introduced in Canada in the 1990s and is still a developing sector in the insurance industry today. Most of the major companies do offer some kind of policy though.

Some plans feature coverage for just one ailment, like cancer (and its many forms), whereas others cover the full 26 illnesses listed above, and sometimes even more. More commonly, carriers will cover the big three—cancer, heart attack, and stroke. The number of covered conditions varies somewhat from company to company. So if you’re looking to cover a specific illness, it’s worth exploring products from a variety of providers.

Putting cost aside, a quick glance at the offerings from most providers shows that critical illness products are often offered in a similar fashion no matter the company, with the biggest differentiator being the number of illnesses covered. However, there are some additional features and benefits you can look for when deciding which policy is best for you.

An interesting feature included in some policies is the partial payout option or—as some companies may call it—“an early discovery benefit”. What this means is that you can receive a small amount of money if you contract a non-life threatening or less-critical illness/condition while insured.

An example of this would be if you develop treatable skin cancer. To the average person this definitely still means the big “C” cancer, however you will not qualify for full payment of the policy benefit amount as most policies do not consider it a “critical illness”. However, if you had a partial payout clause, you’d still receive some money as you did contract a form of cancer listed as eligible, and your policy would carry on through the length of your term.

These partial payout clauses typically payout between 10 to 25 percent of your policy’s value (though generally there is a maximum payout) and most importantly it doesn’t void your policy or reduce your final payout if you do end up subsequently contracting a defined life-threatening critical illness.

These vary between provider and policy, but partial payouts often cover forms of non-life-threatening cancer and coronary angioplasty. The number of covered conditions will typically range between 4 and 16. Some companies will allow for one partial payout while others may allow for multiple partial payouts.

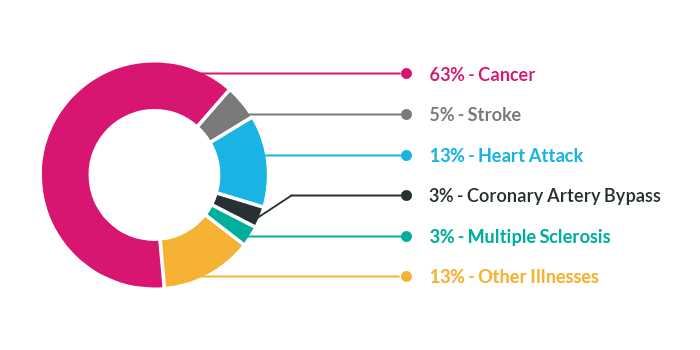

While these numbers may change with time, historically the vast majority of critical illness claims in Canada are for some form of cancer, to the tune of 60 per cent or more. Heart attack and stroke represent the second and third most likely claims, contributing another 20 per cent. It’s known in the industry that these ‘big three’ conditions are the most commonly developed and that’s why you’ll see them offered together in most basic policies.

PolicyAdvisor saves you time and money when comparing Canada’s top life insurance companies. Check it out!

With policies ranging from one illness to 26 or more you might be wondering how many illnesses you should get covered for?

If you want the best protection, you should obviously opt for a policy that covers the entirety of the CLHIA’s standard definitions. While it can be tempting to write off less common diseases as “unlikely to happen to you,” if you do contract one of them, you’ll undoubtedly regret the decision to leave them out of your coverage plan.

However, if premium cost is an issue, or you have a higher risk tolerance, there are some stats worth contemplating.

While these numbers may change with time, historically the vast majority of critical illness claims in Canada are for some form of cancer, to the tune of 60 percent or more. Heart attack and stroke represent the second and third most likely claims, contributing another 20 percent. It’s known in the industry that these “big three” conditions are the most commonly diagnosed and that’s why you’ll see them offered together in most basic policies.

In 2013, the Canadian Life and Health Insurance Association published a standardized list of critical illness definitions (referred to as Critical Illness Benchmark Definitions) in order to help standardize the language around common conditions and afflictions across the industry.

In 2018, the language of these definitions have been updated. Below are the definitions for the following 26 conditions that are widely used in the Canadian insurance industry for critical illness insurance policies, though by no means should this list be considered exhaustive or definitive.

Benign Brain Tumour means a definite Diagnosis of a non-malignant tumour located in the cranial vault and limited to the brain, meninges, cranial nerves or pituitary gland. The tumour must require surgical or radiation treatment or cause Irreversible objective neurological deficit(s).

These deficits must be corroborated by diagnostic imaging showing changes that are consistent in character, location and timing with the neurological deficits.

The Diagnosis of Benign Brain Tumour must be made by a Specialist.

For purposes of the policy, neurological deficits must be detectable by the Specialist and may include, but are not restricted to, measurable loss of hearing, measurable loss of vision, measurable changes in neuro-cognitive function, objective loss of sensation, paralysis, localized weakness, dysarthria (difficulty with pronunciation), dysphasia (difficulty with speech), dysphagia (difficulty swallowing), impaired gait (difficulty walking), difficulty with balance, lack of coordination, or new-onset seizures undergoing treatment. Headache or fatigue will not be considered a neurological deficit.

Exclusions: No benefit will be payable under this condition for:

90-Day Exclusion: No benefit will be payable under this Covered Condition if, within the first 90 days following the later of the Issue Date of an Insured Person’s coverage, or the last Reinstatement Date of an Insured Person’s coverage, such Insured Person has any of the following:

Medical Information about the Diagnosis and any signs, symptoms or investigations leading to the Diagnosis must be reported to the Company within 6 months of the Date of Diagnosis. If this information is not provided within this period, the Company has the right to deny any claim for Benign Brain Tumour or any Critical Illness caused by any Benign Brain Tumour or its treatment.

Cancer (Life-Threatening) means the definite Diagnosis of a malignant tumour. This tumour must be characterized by the uncontrolled growth and spread of malignant cells and the invasion of tissue. Types of cancer include carcinoma, melanoma, leukemia, lymphoma, and sarcoma.

The Diagnosis of Cancer must be made by a Specialist and must be confirmed by a pathology report.

For purposes of the Policy:

Exclusions: No benefit will be payable under this Covered Condition for the following:

No benefit will be payable for the following:

90-Day Exclusion: No benefit will be payable under this Covered Condition if, within the first 90 days following the later of the Issue Date of an Insured Person’s coverage, or the last Reinstatement Date of an Insured Person’s coverage, the Insured Person has any of the following:

Medical Information about the Diagnosis and any signs, symptoms or investigations leading to the Diagnosis must be reported to the Company within 6 months of the Date of Diagnosis. If this information is not provided within this period, the Company has the right to deny any claim for Cancer or any critical illness caused by any cancer or its treatment.

Aortic Surgery means the undergoing of surgery for disease of the aorta requiring excision and surgical replacement of any part of the diseased aorta with a graft. Aorta means the thoracic and abdominal aorta but not its branches. The Surgery must be determined to be medically necessary by a Specialist.

Exclusions: No benefit will be payable under this condition for:

Coronary Artery Bypass Surgery means the undergoing of heart surgery to correct narrowing or blockage of one or more coronary arteries with bypass graft(s). The Surgery must be determined to be medically necessary by a Specialist.

Exclusions: No benefit will be payable under this Covered Condition for:

Heart Attack means a definite diagnosis of the death of heart muscle due to obstruction of blood flow, that results in a rise and fall of biochemical cardiac markers to levels considered diagnostic of myocardial infarction, with at least one of the following:

The diagnosis of Heart Attack (acute myocardial infarction) must be made by a specialist.

Exclusions: No benefit will be payable under this covered condition for:

Heart Valve Replacement or Repair means the undergoing of Surgery to replace any heart valve with either a natural or mechanical valve or to repair heart valve defects or abnormalities. The Surgery must be determined to be medically necessary by a Specialist.

Exclusions: No benefit will be payable under this condition for:

Stroke (Cerebrovascular Accident) means a definite Diagnosis of an acute cerebrovascular event caused by intra-cranial thrombosis or haemorrhage, or embolism from an extra-cranial source, with:

Exclusion: No benefit will be payable under this covered condition for:

Bacterial Meningitis means a definite Diagnosis of meningitis, confirmed by cerebrospinal fluid showing the presence of pathogenic bacteria. The presence of pathogenic bacteria must be confirmed by culture or other generally medically accepted microbiological testing. The Bacterial Meningitis must result in neurological deficits persisting for at least 90 days from the Date of Diagnosis.

The Diagnosis of Bacterial Meningitis must be made by a Specialist.

For purposes of the policy, neurological deficits must be detectable by the Specialist and may include, but are not restricted to, measurable loss of hearing, measurable loss of vision, measurable changes in neuro-cognitive function, objective loss of sensation, paralysis, localized weakness, dysarthria (difficulty with pronunciation), dysphasia (difficulty with speech), dysphagia (difficulty swallowing), impaired gait (difficulty walking), difficulty with balance, lack of coordination, or new-onset seizures undergoing treatment. Headache or fatigue will not be considered a neurological deficit.

Exclusion: No benefit will be payable under this condition for viral meningitis.

Dementia, including Alzheimer’s Disease means a definite Diagnosis of dementia, which must be characterized by a progressive deterioration of memory and at least one of the following areas of cognitive function:

The Insured Person must exhibit:

The Diagnosis of Dementia, including Alzheimer’s Disease must be made by a Specialist.

Exclusion: No benefit will be payable under this Covered Condition for affective or schizophrenic disorders, or delirium.

For purposes of the Policy, reference to the Mini Mental State Exam is to Folstein MF, Folstein SE, McHugh PR, J Psychiatr Res. 1975;12(3):189.

Motor Neuron Disease means a definite Diagnosis of one of the following: amyotrophic lateral sclerosis (ALS or Lou Gehrig’s disease), primary lateral sclerosis, progressive spinal muscular atrophy, progressive bulbar palsy, or pseudo bulbar palsy, and limited to these conditions. The Diagnosis of Motor Neuron Disease must be made by a Specialist.

Multiple Sclerosis means a definite Diagnosis of one of the following occurring after the later of the Issue Date of an Insured Person’s coverage, or the last Reinstatement Date of an Insured Person’s coverage:

Two or more separate clinical attacks, confirmed by a magnetic resonance imaging (MRI) of the nervous system, showing multiple lesions of demyelination;

A single attack, with objective neurological deficits lasting more than 6 months, confirmed by MRI of the nervous system, showing multiple lesions of demyelination; or,

A single attack, confirmed by repeated MRI of the nervous system, which shows multiple lesions of demyelination which have developed at intervals at least one month apart.

The Diagnosis of Multiple Sclerosis must be made by a Specialist.

For purposes of the Policy, neurological deficits must be detectable by a Specialist and may include, but are not restricted to, measurable loss of hearing, measurable loss of vision, measurable changes in neuro-cognitive function, objective loss of sensation, paralysis, localized weakness, dysarthria (difficulty with pronunciation), dysphasia (difficulty with speech), dysphagia (difficulty swallowing), impaired gait (difficulty walking), difficulty with balance, lack of coordination, or new-onset seizures undergoing treatment. Headache or fatigue will not be considered a neurological deficit.

Exclusion: No benefit will be payable for the following:

1-Year Exclusion – No benefit will be payable under this Covered Condition if, within the first year following the later of the Issue Date of an Insured Person’s coverage or the last Reinstatement Date of an Insured Person’s coverage, the Insured Person has any of the following:

Medical information about the Diagnosis and any signs, symptoms or investigations leading to the Diagnosis must be reported to the Company within 6 months of the Date of Diagnosis. If this information is not provided within this period, the Company has the right to deny any claim for Multiple Sclerosis or, any critical illness caused by multiple sclerosis or its treatment.

Parkinson’s Disease and Specified Atypical Parkinsonian Disorders means a definite Diagnosis of either A) Parkinson’s Disease or B) Specified Atypical Parkinsonian Disorders, as defined below.

The Diagnosis of Parkinson’s Disease or a Specified Atypical Parkinsonian Disorder must be made by a Specialist.

Exclusions: No benefit will be payable for Parkinson’s Disease or Specified Atypical Parkinsonian Disorders if, within the first year following the later of the Issue Date or the latest Reinstatement Date of an Insured Person’s coverage, such Insured Person has any of the following:

Medical information about the Diagnosis and any signs, symptoms or investigations leading to the Diagnosis must be reported to the Company within 6 months of the Date of Diagnosis. If this information is not provided within this period, the Company has the right to deny any claim for Parkinson’s Disease or Specified Atypical Parkinsonian Disorders or its treatment.

No benefit will be payable under Parkinson’s Disease and Specified Atypical Parkinsonian Disorders for any other type of Parkinsonism.

Kidney Failure means a definite Diagnosis of chronic Irreversible failure of both kidneys to function, as a result of which regular haemodialysis, peritoneal dialysis or renal transplantation is initiated. The Diagnosis of Kidney Failure must be made by a Specialist.

Major Organ Failure on Waiting List means a definite Diagnosis of the Irreversible failure of the heart, both lungs, liver, both kidneys or bone marrow, and transplantation must be medically necessary. To qualify under Major Organ Failure on Waiting List, the Insured Employee must become enrolled as the recipient in a recognized transplant center in Canada or the United States of America that performs the required form of transplant Surgery. For the purpose of the Survival Period, the Date of Diagnosis is the date of the Insured Employee’s enrolment in the transplant centre. The Diagnosis of the major organ failure must be made by a Specialist.

Major Organ Transplant means a definite Diagnosis of the Irreversible failure of the heart, both lungs, liver, both kidneys or bone marrow and transplantation must be medically necessary. To qualify under Major Organ Transplant, the Insured Person must undergo a transplantation procedure as the recipient of a heart, lung, liver, kidney or bone marrow, and limited to these entities. The Diagnosis of the major organ failure must be made by a Specialist.

Acquired brain injury means a definite diagnosis of new damage to brain tissue caused by traumatic injury, anoxia or encephalitis, resulting in signs and symptoms of neurological impairment that:

The diagnosis of acquired brain injury must be made by a specialist.

Exclusions

No benefit will be payable under this condition for:

Blindness means a definite Diagnosis of the total and Irreversible loss of vision in both eyes, evidenced by:

The Diagnosis of Blindness must be made by a Specialist.

Coma means a definite Diagnosis of a state of unconsciousness with no reaction to external stimuli or response to internal needs for a continuous period of at least 96 hours, and for which period the Glasgow coma score must be 4 or less. The Diagnosis of Coma must be made by a Specialist.

Exclusion: No benefit will be payable under this covered condition for:

Deafness means a definite Diagnosis of the total and Irreversible loss of hearing in both ears, with an auditory threshold of 90 decibels or greater within the speech threshold of 500 to 3,000 hertz. The Diagnosis of Deafness must be made by a Specialist.

Loss of Independent Existence means a definite Diagnosis of the total inability, due to disease or injury, to perform independently, with or without the aid of assistive devices, at least 2 of 6 Activities of Daily Living listed below for a continuous period of at least 90 days with no reasonable chance of recovery. The Diagnosis must be made by a physician and supported by an independent home care assessment made by an occupational therapist or equivalent.

Activities of Daily Living are as follows:

No additional survival period is required once the conditions described above are satisfied.

Loss of Limbs means a definite Diagnosis of the complete severance of two or more limbs at or above the wrist or ankle joint as the result of an accident or medically required amputation. The Diagnosis of Loss of Limbs must be made by a Specialist.

Loss of Speech means a definite Diagnosis of the total and Irreversible loss of the ability to speak as a result of physical injury or disease, for a period of at least 180 days. The Diagnosis of Loss of Speech must be made by a Specialist.

Exclusion: No benefit will be payable under this Covered Condition for all psychiatric related causes.

Paralysis means a definite Diagnosis of the total loss of muscle function of two or more limbs as a result of injury or disease to the nerve supply of those limbs, for a period of at least 90 days following the precipitating event. The Diagnosis of Paralysis must be made by a Specialist.

Severe Burns means a definite Diagnosis of third-degree burns over at least 20% of the body surface. The Diagnosis of Severe Burns must be made by a Specialist.

Aplastic Anemia means a definite Diagnosis of a chronic persistent bone marrow failure, confirmed by biopsy, which results in anemia, neutropenia and thrombocytopenia requiring blood product transfusion, and treatment with at least one of the following:

The Diagnosis of Aplastic Anemia must be made by a Specialist.

Occupational HIV Infection means a definite Diagnosis of infection with Human Immunodeficiency Virus (HIV) resulting from accidental injury during the course of the Insured Person’s normal occupation, which exposed the person to HIV contaminated body fluids.

The accidental injury leading to the infection must have occurred after the later of the Issue Date or latest Reinstatement Date of such Insured Person’s coverage.

Payment under this condition requires satisfaction of all of the following:

The Diagnosis of Occupational HIV Infection must be made by a Specialist.

Exclusion: No benefit will be payable under this covered condition if:

Ultimately, only you can make the decision for what kind of protection you think you need, but due to the unexpected nature of illness, trying to figure out your ‘needs’ can leave you scratching your head. If you’re concerned, it’s best to err on the side of caution.

Try our free critical illness insurance calculator to figure out how much coverage you might require or speak to our friendly advisors.